AREA COUNTIES – Washington County residents averaged about $1.05 in debt for every $1 of income, the lowest 2024 debt-to-income ratio of any county in Vermont.

Caledonia County residents had a debt-to-income ratio of 1.13, while Orleans County residents averaged 1.37 and Lamoille County residents 2.39. Grand Isle County had the highest debt-to-income ratio in the state, with $5.96 in debt for each $1 of income based on Federal Reserve data.

The debt-to-income ratio compares how much debt a person carries with how much income they earn in a year. If the ratio is greater than 1, it means that, on average, people owe more than they earn annually. This can indicate a heavier financial burden and make it harder to keep up with payments.

Debt-to-income ratios vary from county to county within a state because of differences in income levels, housing costs and borrowing habits.

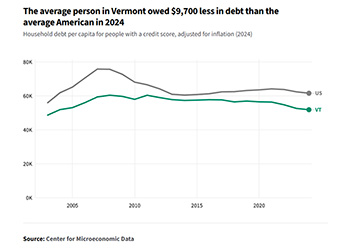

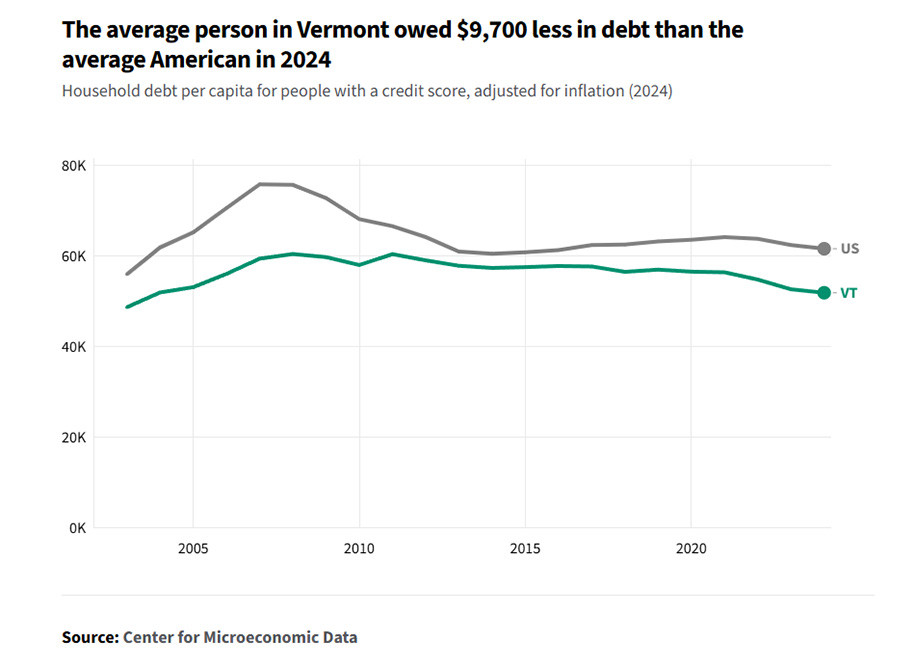

The average person in Vermont owed around $51,900 in 2024. That was $770 less household debt than in 2023, after adjusting for inflation, reflecting slight shifts in household borrowing patterns. according to data from the Center for Microeconomic Data.

Household debt represents the total amount owed by individuals for obligations such as mortgages, student loans, credit cards and auto loans, These figures represent the average debt owed by Vermont residents with a credit score. (Nationally, roughly 80% of adults have a credit score.) While this gives a general sense of the debt burden for Vermont residents, actual individual debt varies — some may carry much more or less debt than this average.

Household debt levels fluctuate over time, especially during times of economic instability. According to the Federal Reserve Bank of New York, household debt increased in the early 2000s, largely driven by housing debts like mortgages. Following the downturn in home prices and the onset of the Great Recession in late 2007, people began paying off their existing loans while taking out fewer new loans, leading to a decline in overall debt levels.

In 2007, during The Great Recession — a debt peak for the US — Vermont residents owed around $16,400 less in household debt than the average American. In 2024, they owed around $9,700 less.

While household debt takes many forms — student loans, auto loans, credit card balances — mortgage debt accounted for around 64.1 percent of all household debt in Vermont in 2024. Mortgages, typically loans taken to purchase homes, are often the largest and longest-term financial commitments for many households. The high cost of housing combined with extended repayment periods (usually five to 30 years) contributes to mortgage debts’ outsized share of overall household debt.

Data in this article was compiled by USAFacts from government sources. USAFacts is a not-for-profit, nonpartisan civic initiative making government data available for all Americans to access and understand.

Paul Fixx is editor of The Hardwick Gazette and lives in Hardwick.